Published on September 1, 2022

RECENT HIGHLIGHTS

- Stocks were down slightly in August as investors weighed the prospects of an aggressive Federal Reserve hiking interest rates against corporate earnings that have been resilient and a healthy labor market.

- Fixed income experienced negative returns as interest rates rose in August, pushing bond prices lower.

- Inflation is finally showing signs of peaking and rolling over from 40-year high levels. The energy sector was the largest contributor to consumer prices declining as oil and gasoline prices have declined the past few months.

- The labor market continues to exhibit strength despite the two quarters of negative Gross Domestic Product (GDP) growth.

August Update

Stocks staged an impressive two-month rally with the S&P 500 Index advancing 17% from the mid-June low to the recent mid-August high. Stocks then traded lower the last two weeks of the month as investors tried to discern how the Federal Reserve will act now that it appears that inflation has peaked. Investors cheered the inflation reports from early-August that showed inflation might have finally peaked and will hopefully begin to trend lower from the 40-year high readings.

The labor market continues to show signs of strength with the most recent employment report showing employers added 528,000 new workers to payrolls, more than double the expectations. Also, the unemployment rate declined to a post-COVID low of 3.5%. We observe that there are over 11 million job openings that employers are attempting to fill.

Second quarter earnings season is nearly completed, and it shows corporations were able to post impressive results that beat expectations for both revenues (up nearly 14% YoY) and earnings (up nearly 9% YoY). We see that expectations for the second half of the year and 2023 exhibit steady growth during these unpredictable times. We believe this is too optimistic and believe expectations will need to come down due to the further slowing in the economy that we expect and the persistently high inflation.

No Fed Meeting, but Plenty of Commentary

There was no Federal Reserve (Fed) meeting in August, and the next one will not be until September 21st. But there were plenty of comments from the Federal Reserve for investors to parse through. These comments came from the Fed’s annual symposium at Jackson Hole where investors were looking for clues as to how much further the current hiking cycle must go. Fed Chairman Jerome Powell stated at this late-August gathering that the central bank will “use our tools forcefully” to bring inflation down from its highest level in over 40 years. He hinted that the Fed would continue to raise interest rates in a way that will cause “some pain” to the economy. We observed that parts of the economy are already slowing down, for example, housing activity has been slowing for a few months now due to higher mortgage rates. The Fed is essentially signaling that fighting inflation is more important than supporting growth at this point.

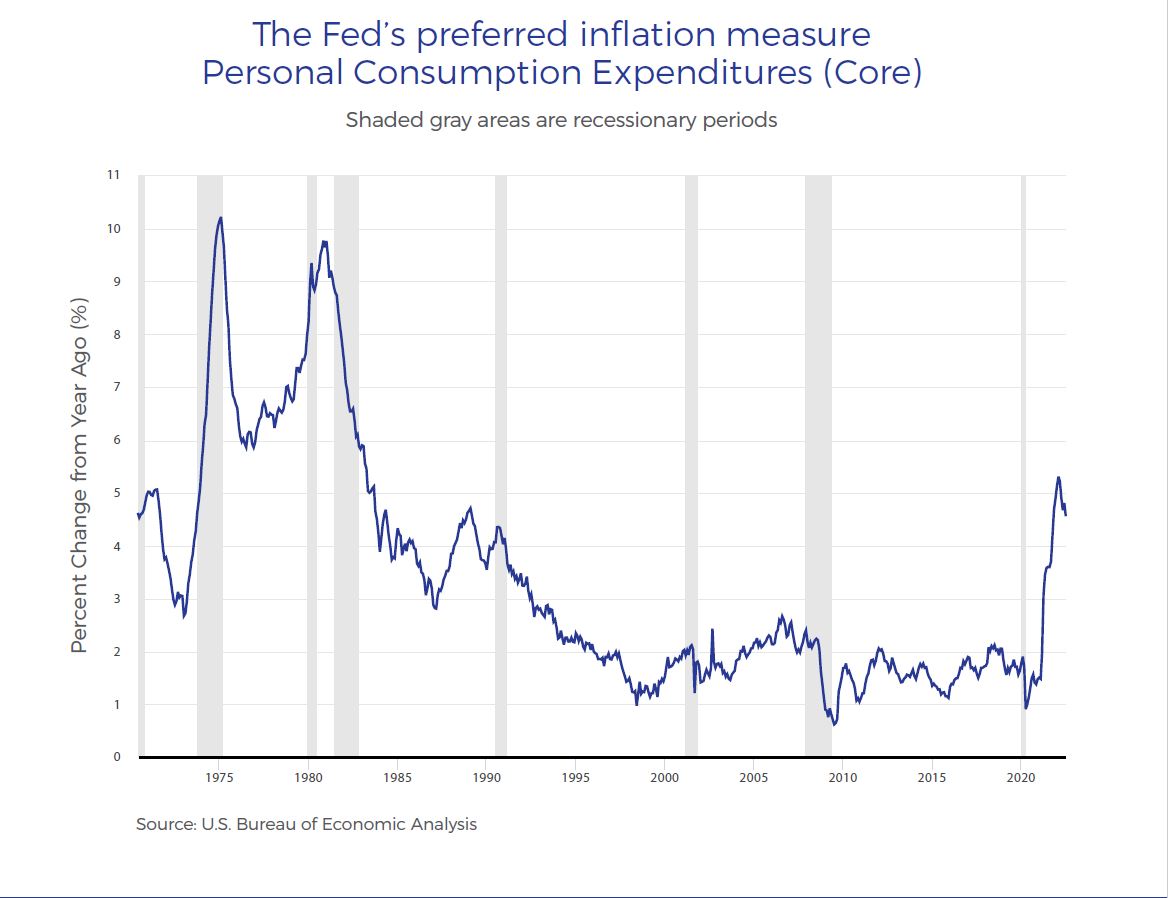

The graph below shows that the Fed’s preferred inflation measure, the Personal Consumption Expenditures (Core), has come down to 4.6% recently, but they indicated this will need to decline to a level near 2% before they let up against their fight with inflation. The good news is that the economy appears to be on solid ground now (labor market healthy, positive earnings growth), but we have concerns that the Fed will push too hard and tip the economy into a recession. Chairman Powell told us they do not want to repeat the mistakes of the 1970’s where they used an on-and-off approach to dealing with inflation. An examination of this period showed that the Fed let up in their fight against inflation in the late-70’s, only to see it roar back again in the early 80’s.

To summarize, the Fed’s approach needs to be restrictive enough, for long enough, to bring inflation down to their 2% target for Personal Consumption Expenditures. The economy is exhibiting pockets of strength and should be able to absorb modest amounts of additional hiking. Future interest rate hikes do not have to be as aggressive as the last two 0.75% hikes because they have already raised fed funds from near zero at the beginning of the year to the current level of 2.25% – 2.50%. We are expecting the Fed to hike interest rates at their September meeting, and a few more times after that, before pausing sometime early next year. It would not surprise us if they begin to cut interest rates in the second half of next year, if inflation comes down and the growth slows in the economy.

Outlook

While corporate earnings remain strong and the labor market is healthy, we are concerned that the high level of inflation will take longer to moderate than originally anticipated. Based on the recent comments by the Fed, it appears clear that they intend to continue increasing interest rates until inflation is under control. While the Fed is trying to engineer a “soft-landing” for the economy we are becoming more concerned that they may in fact drive the economy into a shallow recession. Given this change in outlook we are planning to take advantage of the recent strength in the stock market to de-risk the portfolios by trimming some stock positions. We continue to have a positive long-term outlook for the economy and financial markets, but believe it is appropriate to de-risk the portfolios given all of the short to mid-term uncertainty. We will further detail these portfolio changes shortly in a separate communication piece.

As always, please do not hesitate to contact us if you have any questions and thank you for your continued trust and support.

Important Disclosure Information:

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Richardson Capital Management, LLC [“Richardson”]), or any non-investment related content, made reference to directly or indirectly in this commentary will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this commentary serves as the receipt of, or as a substitute for, personalized investment advice from Richardson. Richardson is neither a law firm, nor a certified public accounting firm, and no portion of the commentary content should be construed as legal or accounting advice. A copy of the Richardson’s current written disclosure Brochure discussing our advisory services and fees continues to remain available upon request or at www.richardson-financial.com. Please Remember: If you are a Richardson client, please contact Richardson, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Richardson account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Richardson accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Note: Limitations: Neither rankings nor recognitions by unaffiliated rating services, publications, media, or other organizations, nor the achievement of any professional designation, certification, degree, or license, membership in any professional organization, or any amount of prior experience or success, should be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if Richardson is engaged, or continues to be engaged, to provide investment advisory services. Rankings published by magazines, and others, generally base their selections exclusively on information prepared and/or submitted by the recognized adviser. Rankings are generally limited to participating advisers (see link as to participation criteria/methodology, to the extent applicable). Unless expressly indicated to the contrary, Richardson did not pay a fee to be included on any such ranking. No ranking or recognition should be construed as a current or past endorsement of Richardson by any of its clients.

ANY QUESTIONS: Richardson’s Chief Compliance Officer remains available to address any questions regarding rankings and/or recognitions, including the criteria used for any reflected ranking.